Credit card debt is one of the most expensive kinds of debt you can carry. The average interest rate in 2026 is hovering around 22%. That means every month you don’t pay it off, it’s growing.

The good news: it’s also one of the most actionable debts to tackle. You don’t need a higher income. You need a plan and some discipline.

Step 1: Know Exactly What You Owe

List every credit card. Write down the balance, the minimum payment, and the interest rate for each one. No estimating. Pull up the actual numbers.

Most people are shocked by the total. That shock is useful. It’s fuel.

Step 2: Stop Adding to the Balance

This sounds obvious. It’s not easy.

Put the cards somewhere inconvenient. Not canceled — you still need the credit history. Just not in your wallet. Delete them from saved browsers. Make spending on them slightly harder than spending cash.

You can’t fill a bucket that has a hole in it.

Step 3: Pick Your Payoff Method

Two proven approaches:

Debt Avalanche: Pay minimums on all cards. Put every extra dollar toward the highest-interest card first. Mathematically fastest. Saves the most money.

Debt Snowball: Pay minimums on all cards. Attack the smallest balance first. Builds momentum through quick wins. Better if you’ve quit payoff plans before.

We cover both in detail in our Debt Avalanche vs. Snowball comparison. Read it and pick one.

Step 4: Find Extra Money to Throw at It

Even $100/month extra makes a massive difference at 22% interest. Where does that $100 come from?

- Cancel subscriptions you forgot you had

- Drop one dining-out habit per week

- Sell something on Facebook Marketplace

- Pick up a few hours of extra work

Run your budget to find the gap. If you don’t have a budget yet, our beginner’s budgeting guide is the right starting point.

Step 5: Consider a Balance Transfer

If your credit score is decent (670+), a 0% balance transfer card can buy you 12–21 months of interest-free payoff time. That’s not magic — you still have to pay it down. But 0% instead of 22% means every payment goes to principal, not interest.

Watch for the transfer fee (usually 3–5%) and set a calendar reminder before the promotional period ends.

Step 6: Automate Minimum Payments Everywhere

A missed payment costs you a late fee plus potential rate hikes. Automate minimums on every card so you never miss one. Then manually make your extra payment to the target card each month.

Step 7: Track Progress Visibly

Write the balance down somewhere you’ll see it. A note on the fridge. A number in your phone. A column in a spreadsheet. Watching it drop is genuinely motivating in a way that keeping it vague never is.

When a card hits zero, don’t lifestyle creep that payment. Roll it straight to the next card. That’s the snowball in action.

How Long Will It Take?

It depends on the balance and how much extra you can throw at it. Here’s a rough guide at 22% interest:

- $3,000 debt + $200 extra/month: ~18 months

- $8,000 debt + $300 extra/month: ~36 months

- $15,000 debt + $400 extra/month: ~50 months

The extra payment amount matters more than almost anything else. Every dollar above the minimum is working 22 cents per year for free.

Start today. Not next month. The interest is running right now.

Once the debt is gone, put that payment toward savings. Build your emergency fund first, then move to investing.

More articles

Debt Payoff

Debt PayoffDebt Avalanche vs. Debt Snowball: Which Method Gets You Out of Debt Faster?

Debt avalanche saves more money. Debt snowball builds momentum. Here's the honest comparison — and how to pick the right method for your personality.

Read → Debt Payoff

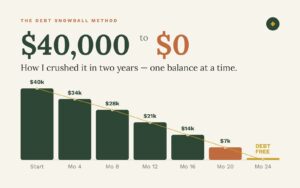

Debt PayoffThe Debt Snowball Method That Crushed My $40k Balance in 2 Years

The debt snowball method helped crush $40k of debt in 2 years. Here's exactly how it works, step by step, and why it actually keeps you going.

Read → Debt Payoff

Debt Payoff