You’ve decided to get out of debt. Good. That’s the hard part.

Now comes the question everyone Googles at 11pm: avalanche or snowball?

Both methods work. But they work differently. And depending on your personality, one will work much better for you than the other.

Here’s the honest breakdown.

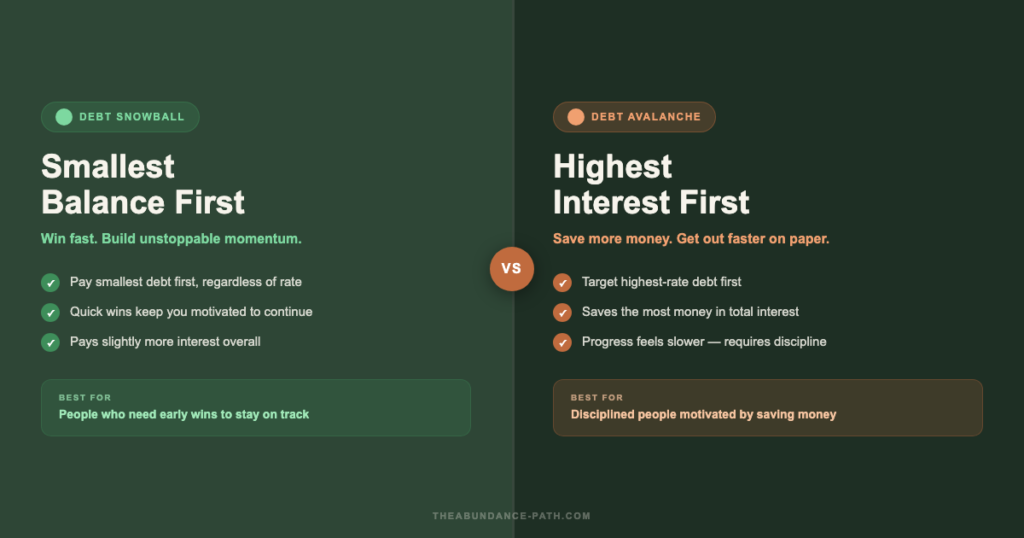

What Is the Debt Snowball Method?

You list all your debts from smallest balance to largest. Then you attack the smallest one first while making minimum payments on everything else.

When the smallest debt is gone, you roll that payment into the next one. Your payment “snowballs” — getting bigger as you go.

Example:

- $400 medical bill

- $2,200 credit card

- $8,500 car loan

- $14,000 student loan

Snowball: pay off the $400 first, regardless of interest rate.

It feels like a win fast. That’s the whole point.

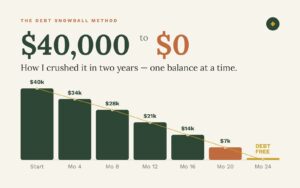

We wrote a full breakdown of this in The Debt Snowball Method That Crushed My $40k Balance in 2 Years — worth reading if you want real numbers.

What Is the Debt Avalanche Method?

You list all your debts from highest interest rate to lowest. You attack the highest-rate debt first while making minimums on the rest.

Same example:

- $2,200 credit card — 24% interest

- $400 medical bill — 0% interest

- $14,000 student loan — 6.5% interest

- $8,500 car loan — 4.9% interest

Avalanche: pay off the credit card first, because it’s costing you the most money every single month.

Mathematically, this is the faster method. You’ll pay less in total interest and get out of debt sooner on paper.

The Real Difference: Math vs. Motivation

The avalanche wins on a spreadsheet. Every time.

But here’s what the spreadsheet doesn’t account for: most people quit.

If your highest-interest debt is also your largest balance, the avalanche can take months before you see any debt disappear. That’s demoralizing. A lot of people lose steam and give up — usually right before it starts working.

The snowball is slower (sometimes by a few hundred dollars). But the early wins keep you going. You cross something off the list. You feel it working. That feeling is powerful.

Dave Ramsey built an empire on this insight. The best debt payoff method is the one you actually finish.

Side-by-Side Comparison

| Debt Snowball | Debt Avalanche | |

|---|---|---|

| Order of payoff | Smallest balance first | Highest interest first |

| Total interest paid | More | Less |

| Time to debt-free | Slightly longer | Slightly faster |

| Motivation | High — quick wins | Lower — slower progress |

| Best for | People who need momentum | Disciplined, numbers-driven people |

Which One Should You Pick?

Ask yourself one question: Have you quit a debt payoff plan before?

If yes — do the snowball. You need the wins. You need to feel progress. The extra interest you’ll pay is worth it if it means you actually finish.

If no — if you’re disciplined, patient, and motivated by numbers — do the avalanche. You’ll save real money and get out faster.

Both methods require the same thing: stop adding to the debt while you pay it down. No new credit card charges you can’t pay off immediately. No new loans. The method doesn’t matter if the balance keeps growing.

A Third Option: The Hybrid

Some people do both.

If you have one or two tiny debts — under $500 — knock those out first for the quick win. Then switch to avalanche order for everything else.

You get the motivational boost of the snowball without sacrificing much mathematically.

It’s not a pure method. But it works for a lot of people.

How to Start Today

Step 1: Write down every debt. Balance, minimum payment, interest rate.

Step 2: Pick your method — snowball or avalanche.

Step 3: Find extra money to throw at your first target. Even $50/month accelerates this faster than you’d expect.

Step 4: Automate minimum payments on everything else so you never miss one.

Step 5: Every time you clear a debt, redirect that full payment to the next one. Don’t lifestyle creep that money away.

The method matters less than starting. Pick one. Start this week.

Read our full guide: How to Get Out of Debt for Good.

The best debt payoff plan is the one you stick with. Pick your method, write down your debts, and make the first extra payment this month.

More articles

Debt Payoff

Debt PayoffThe Debt Snowball Method That Crushed My $40k Balance in 2 Years

The debt snowball method helped crush $40k of debt in 2 years. Here's exactly how it works, step by step, and why it actually keeps you going.

Read → Debt Payoff

Debt PayoffHow to Get Out of Debt for Good: Break Free From the Cycle That’s Keeping You Broke

Read → Debt Payoff

Debt PayoffDebt Consolidation: Does It Actually Help or Make Things Worse?

Debt consolidation sounds like a fix. Sometimes it is. Sometimes it makes things worse. Here's how to tell the difference before you sign anything.

Read →